Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

What are smart contracts? You may have heard this term thrown around a lot lately, but what does it actually mean? A smart contract is a computer program that runs on a blockchain network. It can be used to automate the execution of transactions and agreements between parties. Smart contracts are tamper-proof, secure, and efficient. They have the potential to revolutionize how we do business online.

Smart contract history goes back to 1994 when it was first proposed by computer scientist and legal scholar Nick Szabo. However, it wasn’t until 2009 that the first smart contract was actually executed on the blockchain network Bitcoin.

The DAO was created in 2016 and was responsible for more than $150 million worth of transactions before it was hacked and collapsed later that year.

Smart contracts work with code that is stored on the blockchain. Once a smart contract is created, it cannot be changed or tampered with. This makes them very secure and reliable. The potential uses for smart contracts are endless. They could revolutionize the way we do business.

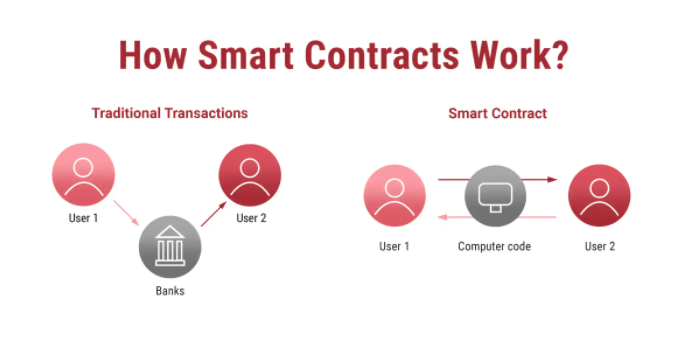

A smart contract is exactly like a traditional contract but it is written in code instead of legal language. The code can be used to create financial agreements between multiple parties that are automatically enforced by the blockchain network.

Although the term “smart contract” might deceive you, they aren’t binding legal agreements. Their main purpose is to automate business logic that performs a variety of operations, processes, or transactions in response to certain criteria. To establish a valid legal connection between this execution and satisfy common contractual conditions between parties, certain procedures must be followed.

Smart contract code is executed by a group of computers called nodes. When a contract is created, it is stored on the blockchain network in an encrypted form. The nodes will then run the program and the smart contract execution instructions.

It utilizes the distributed ledger technology of the blockchain to create an unchangeable record of transactions.

To create smart contracts on the blockchain is a little bit more complicated than this, but the process starts with writing code. An example of this is in a programming language called Solidity, which is designed specifically for Ethereum smart contracts. Once the code has been written and compiled into bytecode, it gets uploaded to the blockchain network where nodes can execute it automatically when certain criteria are met.

The smart contracts are set to receive event notifications from an “oracle,” which is a cryptographically secured streaming data source. The smart contract executes only after it has received the correct combination of events from one or more oracles.

Transaction costs can be added to these oracles as well. These costs would then get distributed among the nodes on the blockchain network that are executing smart contracts in real-time.

How smart contracts are created and executed can be difficult to grasp, being they are so new and revolutionary.

When most people think of smart contracts, the first thing that comes to mind is probably cryptocurrency transactions. For example, Bitcoin is a cryptocurrency that uses a set of predetermined rules called a protocol to verify and record transactions on the blockchain. These rules are implemented in the form of a smart contract.

Another example of other smart contracts is the DAO (Decentralized Autonomous Organization). The DAO was a decentralized venture capital fund that was created through the use of a smart contract.

A simple smart contract can also be used in various programming languages and for more basic purposes, such as verifying someone’s identity or data storage.

Smart contracts are also being used in the music industry. Recently, singer-songwriter Imogen Heap released her single “Tiny Human” using a smart contract on the blockchain network Ethereum virtual machine.

There are a number of cryptocurrencies that have implemented smart contracts into their networks, but the most popular smart contract platform is Ethereum. Ethereum is a decentralized platform that runs smart contract applications. These contracts are written in Solidity, which is a programming language, computerized transaction protocol, specifically designed for creating smart contracts.

Ethereum was created in 2015 by Vitalik Buterin and has since become the second-largest cryptocurrency in terms of market cap.

Other cryptocurrencies that have implemented smart contracts include Bitcoin, NEO, Lisk, and Qtum.

One smart contract use case that is being developed right now is with “The Internet of Things”, or IoT. The goal of this project is to create a network where devices can autonomously interact with each other. This would include things like cars, home appliances, and even clothing.

Consider an instance in which a delivery business, for whatever reason, is unable to complete a delivery. The shipment contains sensors linked to an IoT system. The customer may simply select a new delivery service to pick up the cargo and deliver it, rather than creating a new contract with a new shipping service before the goods can be delivered. Once the shipment’s sensors detect that the goods have arrived, a blockchain-enabled smart contract will execute and complete the transaction between the client and the new delivery firm.

As you can see there are so many use cases with smart contracts and blockchain, the benefits are endless.

Smart contracts offer numerous advantages over traditional legal contracts such as rapid, efficient accuracy, trust, transparency, safety, and cost s0avings. Smart contracts utilize a protocol that automates operations and saves time during various business processes. Automated contract reductions prevent third-party manipulation by eliminating brokers’ and other intermediaries’ obligations. In fact, Smart Contracts don’t use intermediaries. Another benefit of electronic contracts is that the parties to the contract are given full access to the contract’s terms.

This helps to build trust between the parties and avoid any possible disputes or problems with enforcement costs.

The removal of third-party verification also offers cost savings because it eliminates the need for a notary or other expensive legal services. The transparency offered by blockchain technology guarantees that all smart contract activity is public, verifiable, and auditable. This creates a high level of trust among parties.

Smart Contracts are not subject to manipulation by third parties, which means that the two-sided party does not have to worry about their transactions being changed or altered in any way for malicious purposes. The smart contract blockchain provides the highest level of security and data protection with its encryption technology and advanced security features.

There are a number of different smart contract platforms that are currently available. These platforms allow developers to create and deploy smart contracts. The most popular platform we mentioned throughout this blog post is Ethereum, which is a decentralized platform that runs smart contracts.

Other popular platforms include:

Each of these platforms offers its own unique set of features and benefits. Ethereum, for example, is known for its robust programming language, Solidity. Bitcoin is known for its security and stability. NEO offers users the ability to create smart contracts in multiple programming languages.

Smart contract platforms are quickly becoming the go-to choice for businesses and developers who want to take advantage of the benefits offered by these computer programs. The platforms offer a variety of advantages over traditional contracts, including:

Smart contract platforms offer a number of benefits over traditional legal contracts. They can be written in any programming language and deployed on the blockchain as an application or dApp. Smart contract platforms also provide users with real-time updates when it comes to tracking transactions and other events within the network.

Are smart contracts enforceable? This is a question that has been asked quite a bit lately, as the popularity of smart contracts continues to grow. The answer to this question is a bit complicated, as it depends on the specific contract that has been created.

There is no federal contract law in the United States; instead, state courts are responsible for the enforceability and interpretation of contracts. Generally speaking, most smart contracts are considered to be legally binding. This means that if one of the parties involved in the contract does not uphold their end of the bargain, they could be held liable in court. However, there are some exceptions to this rule.

For example, if a party creates a smart contract that is based on illegal activities, then the executed contract may not be legally enforceable. Similarly, if a party creates a smart contract that is found to be fraudulent or misleading, it may not be legally binding.

It is important to note that these are just a few examples of smart contract use cases and that the enforceability of this agreement will vary from case to case. As with any contract, it is always best to consult with an attorney before entering into any agreement.

The smart contracts we use today represent a prototypical example of Amaras Law, the concept that we overestimate technology in the short run compared to the long run. While smart contract development will need evolution in order for them to be widespread in complex commercial relations, it will revolutionize rewards and incentive structures which affect how the parties contract in coming years. To this end, it should be avoided thinking of smart contracts by simply considering the possibility of adapting existing ideas to these new technologies. Rather, we should aim to identify the new ways of conducting business that can be enabled by these technologies.